Sluisweg 10 | 5145 PE Waalwijk | Netherlands +31 416 689 111

Contact us | stahl.com

We welcome your feedback and suggestions regarding this ESG report. Click here to share your input.

Climate resilience

and adaptation

GHG emissions targets

and reduction plan

Case study: taking action

on climate change

Energy use

TOPICS

Greenhouse gas emissions

Michael Costello

Group Director ESG at Stahl

“We're always looking for ways to reduce our emissions. In 2023 Stahl Singapore installed more than 1,800 solar panels, reducing the site's dependence on the main power grid by 40% and reducing its scope 2 emissions.”

Back to top

Tackling climate change is the main focus of our environmental stewardship efforts. We aim to support worldwide efforts to limit global temperature increase to 1.5˚C above pre-industrial levels, by reducing our own impact on the environment while also working with the wider chemicals value chain to help reduce its overall footprint.

Climate change threatens to have a significant impact on our business over the coming decades. We also recognise our own contribution to this critical issue, either directly through our production processes or indirectly through our wider value chain activities. By integrating our climate resilience plans into our core strategy, we believe we can secure our future and be a positive force for climate action in our industry.

The Stahl Climate Resilience and Adaptation Plan sets out our approach to climate risk mitigation, including our ambitious targets and how we plan to achieve them.

Taking action on climate change

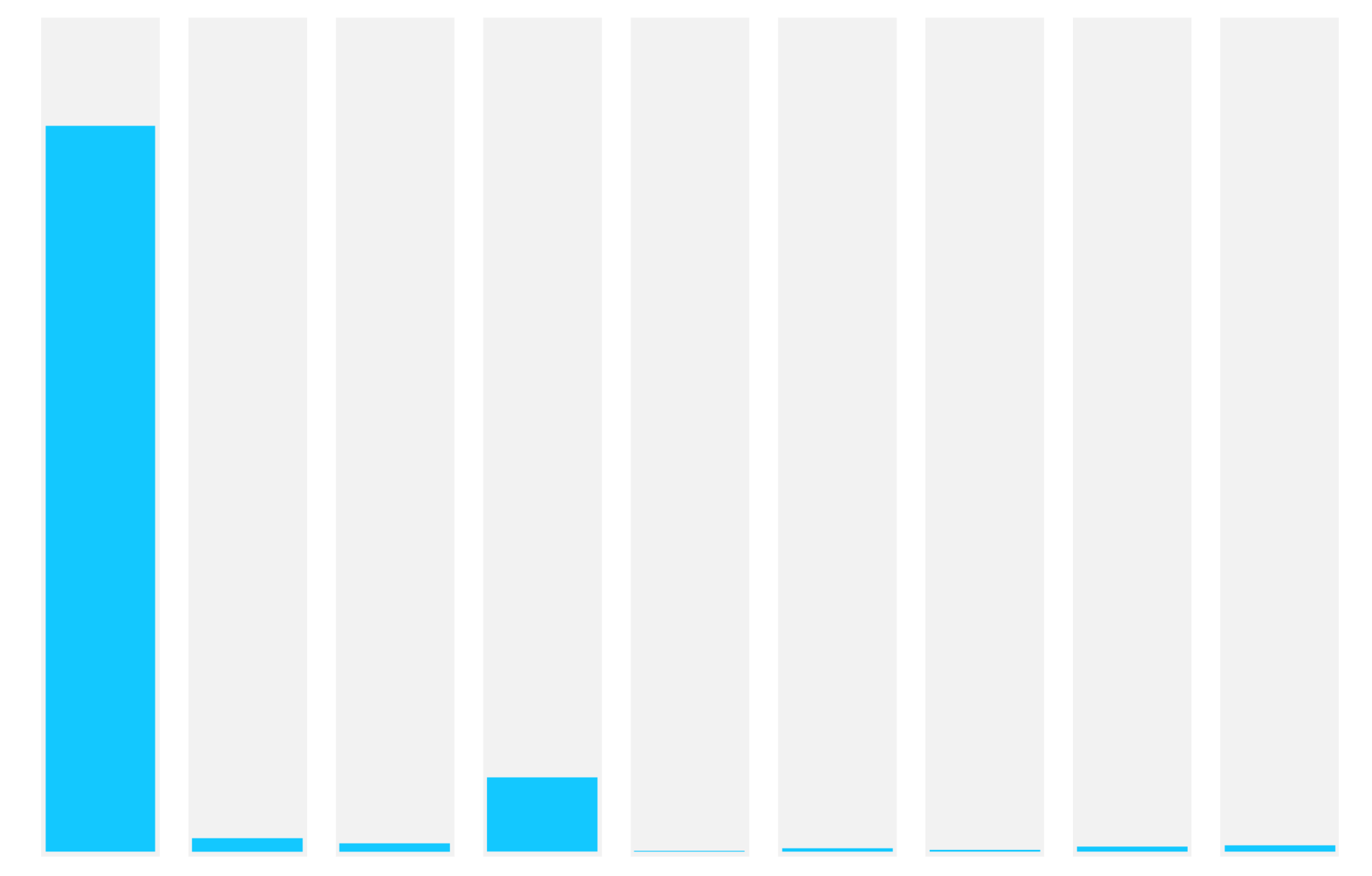

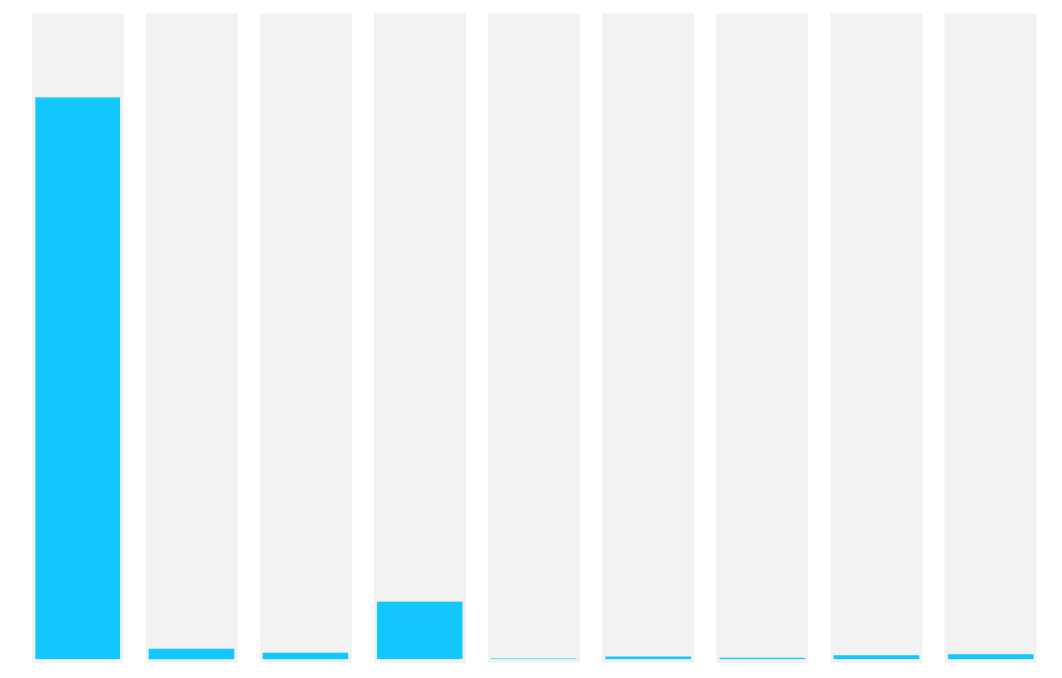

0.7%

0.6%

0.2%

0.4%

0.1%

8.9%

1%

1.6%

86.5%

End-of-life treatment of sold products

Downstream transportation and distribution

Employee commuting

Business travel

Waste generated in operations

Upstream transportation and distribution

Fuel- and energy-related activities

Capital

goods

Purchased goods and services

2023

49%

189,811

0.4315

81,899

Energy intensity (MWh/t)*

Total production volumes

Share of renewable energy

2022

38%

42%

229,533

193,917

0.4345

0.4466

86,594

99,722

2021

Energy consumption

Energy in MWh

*Intensity is related to production volumes, calculated by dividing energy consumption by production volume.

Data verified and validated by Deloitte

Scope 3 categories

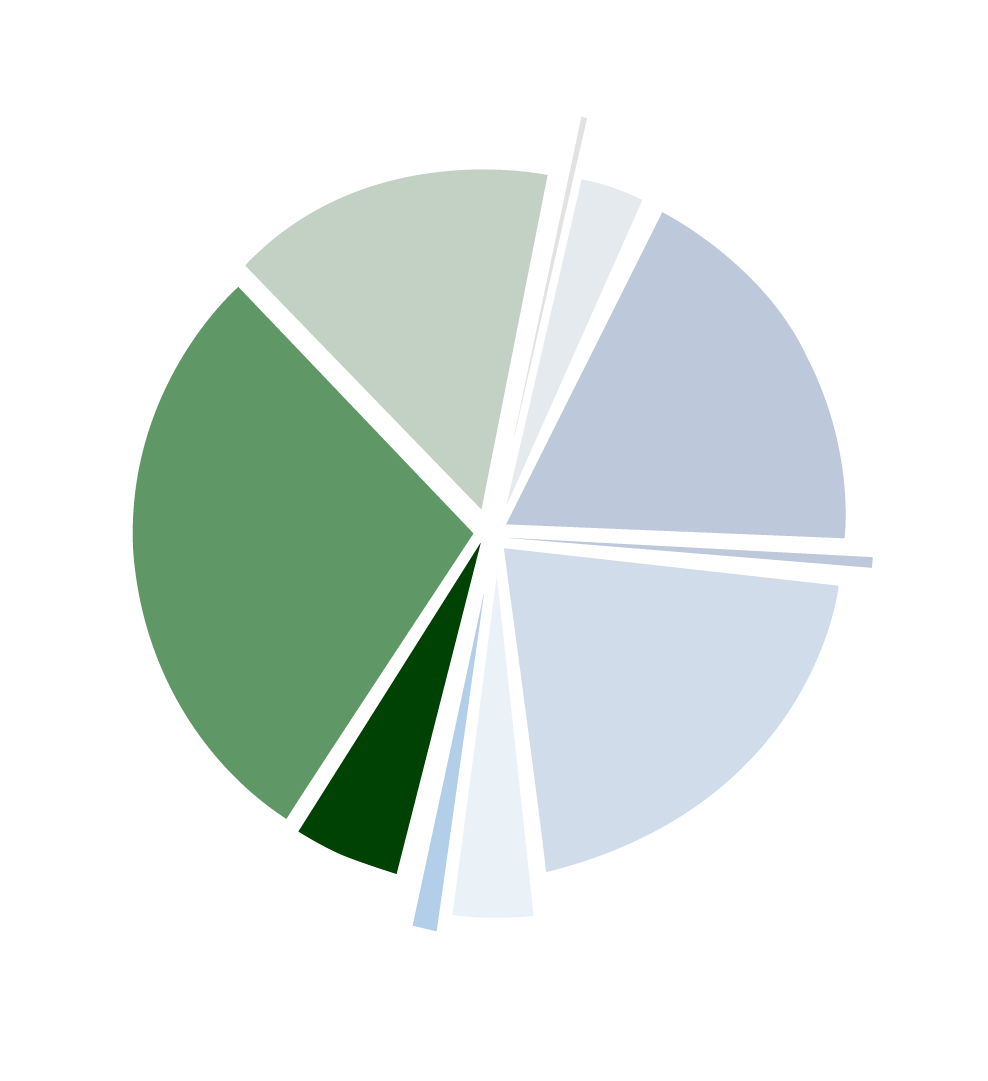

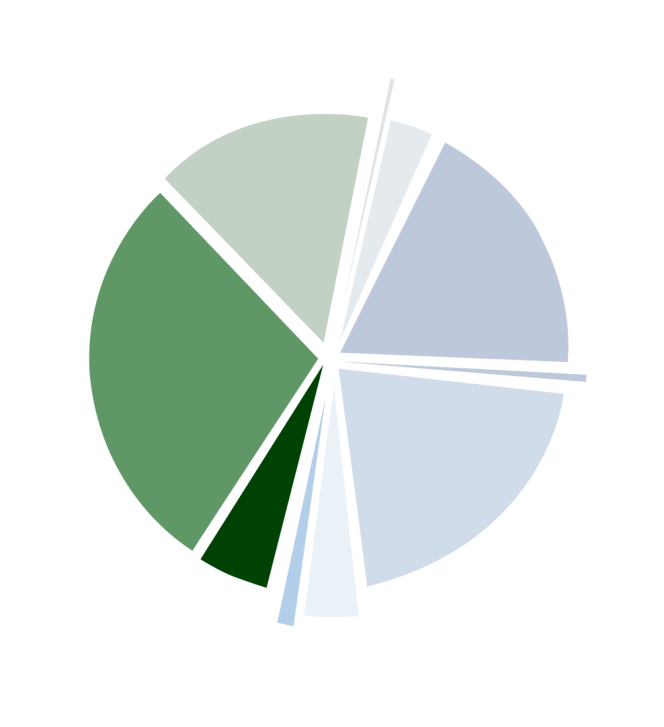

Energy sources

3.8%

0.2%

1.9%

3%

5%

0.6%

15.4%

18.4%

23.2%

28.6%

Purchased renewable electricity 23,395.86 MWh

LPG 478.95 MWh

High-speed diesel (excluding gasoline for FLT)-stationary combustion 2,458.25 MWh

Fuel oil (heating generation etc.) 15,037.40 MWh

Natural gas

(fossil methane)

18,959.98 MWh

Self-generated renewable electricity 4,118,65 MWh

High-speed diesel (gasoline for FLT only)-mobile combustion 203.77 MWh

Steam (purchased)

1,532.66 MWh

Agri briquettes (renewable)

12,637.23 MWh

Purchased electricity - source unknown (mix of grey and renewable)

3,076.73 MWh

Initiating site-based climate resilience assessments

Stahl monitors the long-term impact of climate change on its facilities and is developing resilience against potential climate- and weather-related events. In 2023, we introduced and implemented a new methodology to assess risk at Stahl sites around the world and define mitigation actions and investments.

Our approach is based on implementing individual climate resilience assessments at Stahl's production sites and Centres of Excellence. The assessments are based on studies conducted by the sustainability consultancy ERM, which model potential climate-related scenarios for 2030 and 2050. The scenarios present a range of physical, climate-related risks, from extreme heat and cold to flooding and water scarcity.

The individual site assessments were completed by Stahl’s regional manufacturing site teams using Sphera software. The potential impact of climate-related events on each site, including the impact on the site's infrastructure and operations, was evaluated. The assessments also defined the likely time frame for these events to occur.

The site-based risk assessments completed in 2023 will be reviewed and updated periodically over the coming years to reflect changes in climate projections and to take into account potential severe weather events at our sites.

Maarten Heijbroek

CEO of Stahl

“Aligning our emissions reduction targets with the Paris Agreement goals, and securing validation from the Science Based Targets initiative, are ambitious goals that will require continuous technological advances throughout the value chain. We're already working closely with our upstream partners to reach the 10-year milestone, and we will report on our progress in future ESG reports.”

Dennis Koh

General Manager Stahl Singapore

“We're always looking for ways to reduce our emissions. In 2023, Stahl Singapore installed more than 1,800 solar panels, reducing the sites’ dependence on the main power grid by 40% and reducing scope 2 emissions.”

[1] The target boundary includes biogenic land-related emissions and removals from bio-energy feedstocks

Reduce absolute scope 3 GHG emissions (from upstream purchased goods and services) by 25% vs 2021 base year.

Reduce absolute scope 1, 2

GHG emissions by 42% by 2030 vs 2021 base year. [1]

Secure our future and be a positive force for climate action in our industry.

RESULT

1) Reduce direct and indirect GHG emissions,

2) Establish a scope 3 emissions target,

3) Establish a climate resilience and adaption plan for the company, and

4) Track and report on our progress vs targets.

APPROACH

"Tackling climate change is the main focus of our environmental stewardship efforts. We aim to support worldwide efforts to limit global temperature increase to 1.5˚C above pre-industrial levels by reducing our own impact on the environment while also working with the wider chemicals value chain to help reduce its overall footprint."

Serena Portella

Support limiting global temperature increase to 1.5˚C above pre-industrial levels

GOAL

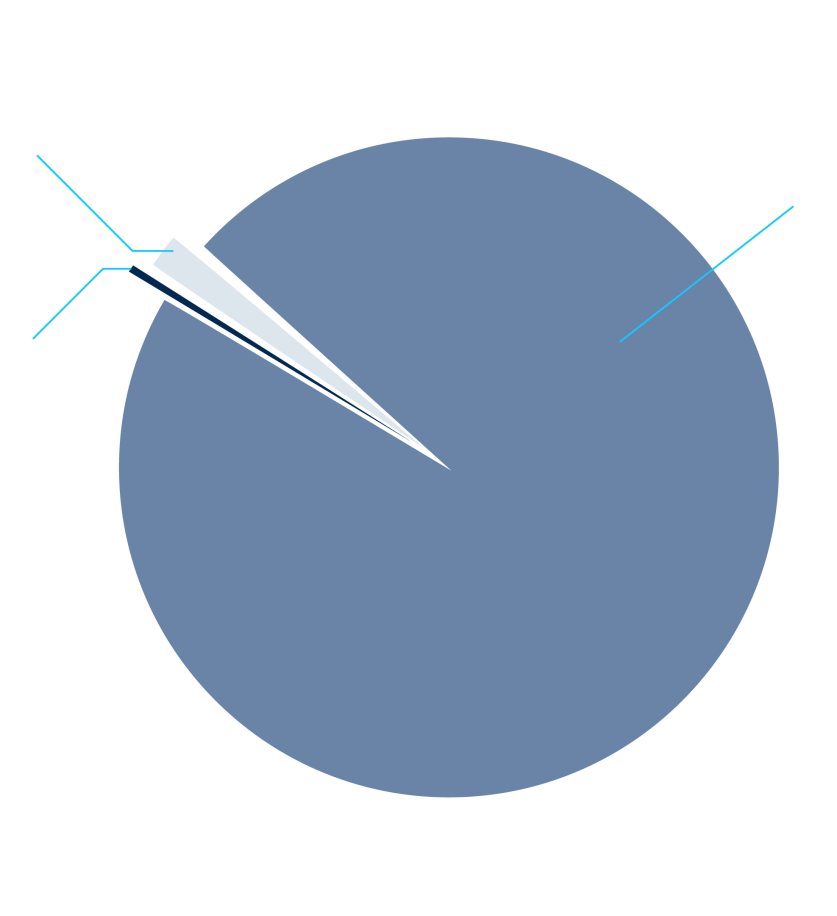

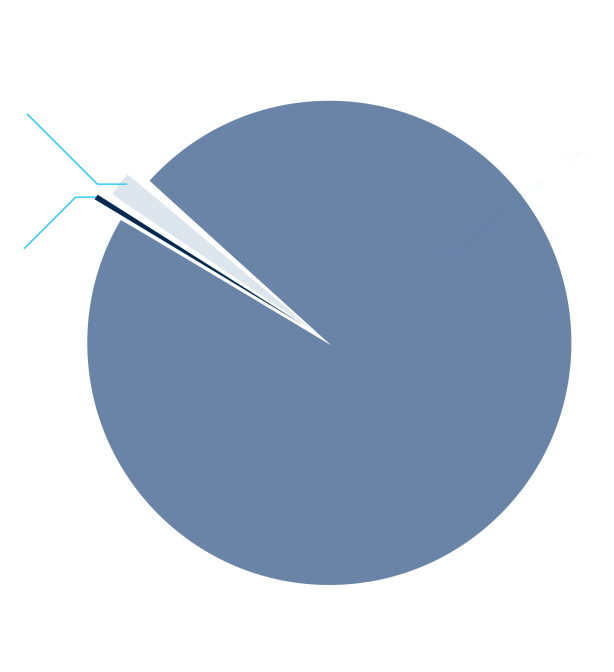

Scope 3

630,557

98%

Scope 1

10,453

1.6%

Scope 2

2,127

0.3%

Complete scope 1, 2 and 3 emissions for 2023 (tCO2e)

Data for Scope1 and 2 verified and validated by Deloitte

We have already incorporated climate resilience into our strategy and operations. In 2023, we built a climate change matrix to assess climate-related risks, based on a range of studied scenarios, and calculated their potential financial impact.

Stahl’s Climate Resilience and Adaptation Plan ensures that we take action on climate risks and adapt to the impacts of climate change. The plan is structured around the following two categories of risk:

Climate Resilience AND

Adaptation Plan

Stahl reassessed all 15 GHG scope 3 emissions categories with the help of an external consultant. This provided an accurate understanding of how our scope 3 emissions are generated and formed the foundation for setting our scope 3 emissions reduction target (see above).

Improving calculations

and reporting

The Greenhouse Gas Protocol is the most widely used international framework for carbon accounting. It categorises greenhouse gas emissions into three ‘scopes’. Scope 1 covers direct emissions from owned or directly controlled sources (e.g., factories and vehicles). Scope 2 covers indirect emissions from the generation of purchased electricity, steam, heating and cooling consumed. Scope 3 includes all indirect emissions that occur within a company’s value chain, both upstream and downstream.

for example, the possible impact of more extreme weather events on Stahl’s manufacturing locations and strategic Centres of Excellence.

including policy changes (carbon tax, fossil tax), reputational impacts and shifts in market preferences, norms and technologies that are linked to the transition towards a low-carbon economy.

Physical risks

Transitioning risks

Estimation of scope 3 (indirect) emissions

Change

2023

-5.96%

-8%

3.32

630,557

CO2e intensity – scope 3 (tCO2e/ton produced)

2022

3.92

3.53

685,441

898,888

2021

CO2e emissions – scope 3 (tCO2e)

The SBTi classifies emissions reduction targets according to two potential temperature pathways: 1) limiting global temperature rises to 1.5°C above pre-industrial levels, and 2) limiting temperature rises to well below 2°C. Stahl’s scope 1 and 2 target is aligned with the 1.5°C trajectory, while the scope 3 target was validated under the 2°C pathway.

Stahl has put a plan in place to ensure that our scope 1, 2 and 3 targets are achieved. This plan is tracked regularly and monitored. Examples of the steps being taken include:

ESG ROADMAP 2030

GREENHOUSE GAS EMISSIONS

RENEWABLE ENERGY

The proportion of renewable energy within Stahl’s overall energy consumption mix reached 49% in 2023, an increase of 16% compared to 2022. This was due to our continued investment in solar panels and the ongoing transition to renewable electricity. In Europe, 100% of our manufacturing sites are purchasing renewable electricity. Outside of Europe, our sites in Brazil and Singapore also purchase 100% renewable electricity.

Stahl has established near-term, science-based targets to reduce its greenhouse gas emissions.

These targets were validated by the Science Based Targets initiative (SBTi) in 2023. These targets commit Stahl to:

reduction targets

2023 progress (on target):

solar panels installed at 4 sites

2030 goal:

6 sites using on-site renewable sources (minimum 20% of total energy usage)

Data verified and validated by Deloitte

In 2023, Stahl’s scope 1 absolute emissions fell by 12% vs 2022 (10,453 tCO₂e vs 11,852 tCO₂e in 2022),

mainly because of energy efficiency investment and lower production volumes.

Scope 2 absolute emissions dropped by 54% (2,127 tCO₂e versus 4,617 tCO₂e in 2022), mainly as a result of our investment in solar panels and switching to renewable energy from national grids.

Greenhouse gas emissions Stahl

The following actions are being taken to reduce Stahl’s scope 1 and 2 emissions:

Continued sourcing of renewable energy at our manufacturing sites,

Improving the efficiency of equipment, such as boilers, reactors and condensers,

Electrification of energy and equipment, where feasible, and

On-site renewable energy generation, such as solar panels, already installed at four Stahl sites – Brazil, Mexico, India and Singapore (2023).

The following actions are being taken to reduce Stahl’s scope 3 emissions:

Replacing fossil fuel-based raw materials with lower-carbon alternatives, such as renewable carbon-based feedstocks,

Low-carbon raw materials used in all new product development,

Raw Material Working Groups established per material or category, focused on introducing selected low-carbon alternatives to replace higher-carbon versions,

Continuously improving the quality of raw material CO₂ emissions data based on verified LCA methodologies and the Ecoinvent database, and

Focus on the top raw material categories, according to their GHG impact (i.e., purchased volume x emission factor).

Scope 3 GHG emissions (CO₂, CH4, N2O, HFCs, PFCs, and SF6) are reported in metric tons of CO₂ equivalent (CO₂e), excluding biogenic CO₂ emissions and are independent of any GHG trading schemes, such as purchases, sales or transfers of offsets or allowances.

In 2023, Stahl’s largest scope 3 category was Purchased goods and services (category 1), which includes everything the company sources from its suppliers. The decrease in scope 3 emissions in 2023 (-8% compared to 2022) is due to reduced purchased goods and services, improvement of LCA data quality and the sourcing of raw materials with a lower carbon footprint. Our scope 3 emissions are expected to increase in 2024, due to the associated emissions from Stahl’s acquisition of ICP Industrial Solutions Group in 2023.

Managing indirect emissions from our value chain (scope 3)

Reported scope 1 and 2 include emissions from Stahl’s 11 manufacturing sites, excluding the ICP Industrial Solutions Group locations acquired in 2023.

Note: non-manufacturing Stahl locations, such as offices, labs and home offices, were excluded from the 2023 reported GHG emissions.

2023 saw the extension of Stahl's on-site renewable energy programme, with the addition of new solar panels at our manufacturing facility in Singapore, the fourth of its kind since 2020 (following Brazil, Mexico and India). This keeps us on track to achieve our 2030 target of six sites powered by renewable energy sources.

Stahl’s facilities in Italy and Mexico completed the installation of solar water heaters in 2023, which reduced their use of fossil fuels to heat water for production and hygiene purposes compared to previous years.

POWERING OUR SITES WITH SOLAR ENERGY

Addressing climate change is the number one priority for all stakeholders across the coatings and treatments value chain. Stahl achieved significant reductions in GHG emissions since the Paris Agreement was signed in 2015 (43% absolute scope 1 and 2 emissions reduction achieved between 2015 and 2021).

An ambitious emissions reduction target was submitted to the Science Based Targets initiative (SBTi) in 2022, and this was validated and published on the SBTi website in 2023.

Achieving our GHG targets will be challenging, since many of the activities in the value chain take place upstream, beyond our direct influence. However, we have built the foundations to get there.

As a founding member of the Renewable Carbon Initiative (RCI), we play a key role in supporting the de-fossilisation of the chemicals value chain and its transition to renewable feedstocks. We are investing significant resources in measuring the footprint of our raw materials and products using life cycle assessment (LCA) methodology. We are also working to secure the most relevant supply chain certifications for our low-carbon technology materials, such as RedCert² and ISCC PLUS.

As we build on this momentum, we have a key milestone firmly in our sights. 2030 will mark the 100th anniversary of Stahl. It is also the end point of our ESG Roadmap to 2030, by which time we expect to have achieved our mid-term ESG targets. More importantly, by the end of this decade, we expect to see the wider chemicals industry making more significant progress towards de-fossilisation than in the previous 30 years, with Stahl acting as a driving force in our markets.

Collaboration will be key. By working together – as one value chain – we believe the chemical industry can be part of the solution for mitigating climate change, reversing the global warming trend, and progressively reducing biodiversity loss.

This section of our report follows our climate change ambitions and our recent efforts to reduce the environmental impact of Stahl and its value chain partners.

Stahl’s energy consumption relates primarily to the production processes used to make our speciality coating and treatment products. We continue to invest in cleaner and renewable energy sources and to further reduce our energy consumption. The largest potential improvement area for reducing GHG emissions is linked to the purchase of raw materials.

EMISSIONS

Sluisweg 10 | 5145 PE Waalwijk | Netherlands +31 416 689 111

Contact us | stahl.com

We welcome your feedback and suggestions regarding this ESG report. Click here to share your input.

Back to top

Initiating site-based climate resilience assessments

Stahl monitors the long-term impact of climate change on its facilities and is developing resilience against potential climate- and weather-related events. In 2023, we introduced and implemented a new methodology to assess risk at Stahl sites around the world and define mitigation actions and investments.

Our approach is based on implementing individual climate resilience assessments at Stahl's production sites and Centres of Excellence. The assessments are based on studies conducted by the sustainability consultancy ERM, which model potential climate-related scenarios for 2030 and 2050. The scenarios present a range of physical, climate-related risks, from extreme heat and cold to flooding and water scarcity.

The individual site assessments were completed by Stahl’s regional manufacturing site teams using Sphera software. The potential impact of climate-related events on each site, including the impact on the site's infrastructure and operations, was evaluated. The assessments also defined the likely time frame for these events to occur.

The site-based risk assessments completed in 2023 will be reviewed and updated periodically over the coming years to reflect changes in climate projections and to take into account potential severe weather events at our sites.

We have already incorporated climate resilience into our strategy and operations. In 2023, we built a climate change matrix to assess climate-related risks, based on a range of studied scenarios, and calculated their potential financial impact.

for example, the possible impact of more extreme weather events on Stahl’s manufacturing locations and strategic Centres of Excellence.

including policy changes (carbon tax, fossil tax), reputational impacts and shifts in market preferences, norms and technologies that are linked to the transition towards a low-carbon economy.

Physical risks

Transitioning risks

"Tackling climate change is the main focus of our environmental stewardship efforts. We aim to support worldwide efforts to limit global temperature increase to 1.5˚C above pre-industrial levels by reducing our own impact on the environment while also working with the wider chemicals value chain to help reduce its overall footprint."

Serena Portella

Stahl’s Climate Resilience and Adaptation Plan ensures that we take action on climate risks and adapt to the impacts of climate change. The plan is structured around the following two categories of risk:

Climate Resilience AND

Adaptation Plan

Tackling climate change is the main focus of our environmental stewardship efforts. We aim to support worldwide efforts to limit global temperature increase to 1.5˚C above pre-industrial levels, by reducing our own impact on the environment while also working with the wider chemicals value chain to help reduce its overall footprint.

Secure our future and be a positive force for climate action in our industry.

RESULT

1) Reduce direct and indirect GHG emissions,

2) Establish a scope 3 emissions target,

3) Establish a climate resilience and adaption plan for the company, and

4) Track and report on our progress vs targets.

APPROACH

Support limiting global temperature increase to 1.5˚C above pre-industrial levels

GOAL

Climate change threatens to have a significant impact on our business over the coming decades. We also recognise our own contribution to this critical issue, either directly through our production processes or indirectly through our wider value chain activities. By integrating our climate resilience plans into our core strategy, we believe we can secure our future and be a positive force for climate action in our industry.

The Stahl Climate Resilience and Adaptation Plan sets out our approach to climate risk mitigation, including our ambitious targets and how we plan to achieve them.

Taking action on climate change

Maarten Heijbroek

CEO of Stahl

“Aligning our emissions reduction targets with the Paris Agreement goals, and securing validation from the Science Based Targets initiative, are ambitious goals that will require continuous technological advances throughout the value chain. We're already working closely with our upstream partners to reach the 10-year milestone, and we will report on our progress in future ESG reports.”

Stahl reassessed all 15 GHG scope 3 emissions categories with the help of an external consultant. This provided an accurate understanding of how our scope 3 emissions are generated and formed the foundation for setting our scope 3 emissions reduction target (see above).

Improving calculations

and reporting

0.7%

0.6%

0.2%

0.4%

0.1%

8.9%

1%

1.6%

86.5%

End-of-life treatment of sold products

Employee commuting

Downstream transportation and distribution

Waste generated in operations

Upstream transportation and distribution

Fuel- and energy-related activities

Purchased goods and services

Business travel

Capital goods

Scope 3 categories

Scope 3 GHG emissions (CO₂, CH4, N2O, HFCs, PFCs, and SF6) are reported in metric tons of CO₂ equivalent (CO₂e), excluding biogenic CO₂ emissions and are independent of any GHG trading schemes, such as purchases, sales or transfers of offsets or allowances.

In 2023, Stahl’s largest scope 3 category was Purchased goods and services (category 1), which includes everything the company sources from its suppliers. The decrease in scope 3 emissions in 2023 (-8% compared to 2022) is due to reduced purchased goods and services, improvement of LCA data quality and the sourcing of raw materials with a lower carbon footprint. Our scope 3 emissions are expected to increase in 2024, due to the associated emissions from Stahl’s acquisition of ICP Industrial Solutions Group in 2023.

Estimation of scope 3 (indirect) emissions

2021

3.92

898,888

CO2e intensity – scope 3 (tCO2e/ton produced)

CO2e emissions – scope 3 (tCO2e)

Estimation of scope 3 (indirect) emissions

2022

3.53

685,441

CO2e intensity – scope 3 (tCO2e/ton produced)

CO2e emissions – scope 3 (tCO2e)

Change

-5,96%

-8%

CO2e intensity – scope 3 (tCO2e/ton produced)

CO2e emissions – scope 3 (tCO2e)

Estimation of scope 3 (indirect) emissions

2023

3.32

630,557

CO2e intensity – scope 3 (tCO2e/ton produced)

CO2e emissions – scope 3 (tCO2e)

Complete scope 1, 2 and 3 emissions for 2023 (tCO2e)

Data for Scope 1 and 3

verified and validated by Deloitte

Scope 3

630,557

98%

Scope 1

10,453

1.6%

Scope 2

2,127

0.3%

[1] The target boundary includes biogenic land-related emissions and removals from bio-energy feedstocks

Reduce absolute scope 3 GHG emissions (from upstream purchased goods and services) by 25% vs 2021 base year.

2030 goal:

6 sites using on-site renewable sources (minimum 20% of total energy usage)

2023 progress

(on target):

solar panels installed at 4 sites

Reduce absolute scope 1, 2

GHG emissions by 42% by 2030 vs 2021 base year. [1]

3.8%

0.2%

1.9%

3%

5%

15.4%

18.4%

23.2%

28.6%

28.6%

Purchased renewable electricity 23,395.86 MWh

0,6%

LPG 478.95 MWh

3%

High-speed diesel (excluding gasoline for FLT)-stationary combustion 2,458.25 MWh

18,4%

Fuel oil (heating generation etc.) 15,037.40 MWh

23,2%

Natural gas (fossil methane)

18,959.98 MWh

5%

Self-generated renewable electricity 4,118,65 MWh

0,2%

High-speed diesel (gasoline for FLT only)-mobile combustion 203.77 MWh

1,9%

Steam (purchased)

1,532.66 MWh

15,4%

Agri briquettes (renewable)

12,637.23 MWh

3,8%

Purchased electricity - source unknown (mix of grey and renewable)

3,076.73 MWh

Energy sources

Dennis Koh

General Manager Stahl Singapore

“We're always looking for ways to reduce our emissions. In 2023, Stahl Singapore installed more than 1,800 solar panels, reducing the sites’ dependence on the main power grid by 40% and reducing scope 2 emissions.”

2021

38%

229,533

0.4345

99,722

Energy intensity (MWh/t)*

Total production volumes

Share of renewable energy

Energy in MWh

2022

42%

193,917

0.4466

86,594

Energy intensity (MWh/t)*

Total production volumes

Share of renewable energy

Energy in MWh

2023

49%

189,811

0.4315

81,899

Energy intensity (MWh/t)*

Total production volumes

Share of renewable energy

Energy in MWh

Energy consumption

*Intensity is related to production volumes, calculated by dividing energy consumption by production volume.

Data verified and validated by Deloitte

2023 saw the extension of Stahl's on-site renewable energy programme, with the addition of new solar panels at our manufacturing facility in Singapore, the fourth of its kind since 2020 (following Brazil, Mexico and India). This keeps us on track to achieve our 2030 target of six sites powered by renewable energy sources.

Stahl’s facilities in Italy and Mexico completed the installation of solar water heaters in 2023, which reduced their use of fossil fuels to heat water for production and hygiene purposes compared to previous years.

POWERING OUR SITES WITH SOLAR ENERGY

The Greenhouse Gas Protocol is the most widely used international framework for carbon accounting. It categorises greenhouse gas emissions into three ‘scopes’. Scope 1 covers direct emissions from owned or directly controlled sources (e.g., factories and vehicles). Scope 2 covers indirect emissions from the generation of purchased electricity, steam, heating and cooling consumed. Scope 3 includes all indirect emissions that occur within a company’s value chain, both upstream and downstream.

Managing indirect emissions from our value chain (scope 3)

RENEWABLE ENERGY

The proportion of renewable energy within Stahl’s overall energy consumption mix reached 49% in 2023, an increase of 16% compared to 2022. This was due to our continued investment in solar panels and the ongoing transition to renewable electricity. In Europe, 100% of our manufacturing sites are purchasing renewable electricity. Outside of Europe, our sites in Brazil and Singapore also purchase 100% renewable electricity.

Reported scope 1 and 2 include emissions from Stahl’s 11 manufacturing sites, excluding the ICP Industrial Solutions Group locations acquired in 2023.

Note: non-manufacturing Stahl locations, such as offices, labs and home offices, were excluded from the 2023 reported GHG emissions.

The following actions are being taken to reduce Stahl’s scope 1 and 2 emissions:

Continued sourcing of renewable energy at our manufacturing sites,

Improving the efficiency of equipment, such as boilers, reactors and condensers,

Electrification of energy and equipment, where feasible, and

On-site renewable energy generation, such as solar panels, already installed at four Stahl sites – Brazil, Mexico, India and Singapore (2023).

The following actions are being taken to reduce Stahl’s scope 3 emissions:

Replacing fossil fuel-based raw materials with lower-carbon alternatives, such as renewable carbon-based feedstocks,

Low-carbon raw materials used in all new product development,

Raw Material Working Groups established per material or category, focused on introducing selected low-carbon alternatives to replace higher-carbon versions,

Continuously improving the quality of raw material CO₂ emissions data based on verified LCA methodologies and the Ecoinvent database, and

Focus on the top raw material categories, according to their GHG impact (i.e., purchased volume x emission factor).

In 2023, Stahl’s scope 1 absolute emissions fell by 12% vs 2022 (10,453 tCO₂e vs 11,852 tCO₂e in 2022),

mainly because of energy efficiency investment and lower production volumes.

Scope 2 absolute emissions dropped by 54% (2,127 tCO₂e versus 4,617 tCO₂e in 2022), mainly as a result of our investment in solar panels and switching to renewable energy from national grids.

Greenhouse gas emissions Stahl

Greenhouse gas emissions Stahl

Greenhouse gas emissions Stahl

Data verified and validated by Deloitte

GREENHOUSE GAS EMISSIONS

The SBTi classifies emissions reduction targets according to two potential temperature pathways: 1) limiting global temperature rises to 1.5°C above pre-industrial levels, and 2) limiting temperature rises to well below 2°C. Stahl’s scope 1 and 2 target is aligned with the 1.5°C trajectory, while the scope 3 target was validated under the 2°C pathway.

Stahl has put a plan in place to ensure that our scope 1, 2 and 3 targets are achieved. This plan is tracked regularly and monitored. Examples of the steps being taken include:

Stahl’s energy consumption relates primarily to the production processes used to make our speciality coating and treatment products. We continue to invest in cleaner and renewable energy sources and to further reduce our energy consumption. The largest potential improvement area for reducing GHG emissions is linked to the purchase of raw materials.

Stahl has established near-term, science-based targets to reduce its greenhouse gas emissions.

These targets were validated by the Science Based Targets initiative (SBTi) in 2023. These targets commit Stahl to:

reduction targets

Addressing climate change is the number one priority for all stakeholders across the coatings and treatments value chain. Stahl achieved significant reductions in GHG emissions since the Paris Agreement was signed in 2015 (43% absolute scope 1 and 2 emissions reduction achieved between 2015 and 2021).

An ambitious emissions reduction target was submitted to the Science Based Targets initiative (SBTi) in 2022, and this was validated and published on the SBTi website in 2023.

Achieving our GHG targets will be challenging, since many of the activities in the value chain take place upstream, beyond our direct influence. However, we have built the foundations to get there.

As a founding member of the Renewable Carbon Initiative (RCI), we play a key role in supporting the de-fossilisation of the chemicals value chain and its transition to renewable feedstocks. We are investing significant resources in measuring the footprint of our raw materials and products using life cycle assessment (LCA) methodology. We are also working to secure the most relevant supply chain certifications for our low-carbon technology materials, such as RedCert² and ISCC PLUS.

As we build on this momentum, we have a key milestone firmly in our sights. 2030 will mark the 100th anniversary of Stahl. It is also the end point of our ESG Roadmap to 2030, by which time we expect to have achieved our mid-term ESG targets. More importantly, by the end of this decade, we expect to see the wider chemicals industry making more significant progress towards de-fossilisation than in the previous 30 years, with Stahl acting as a driving force in our markets.

Collaboration will be key. By working together – as one value chain – we believe the chemical industry can be part of the solution for mitigating climate change, reversing the global warming trend, and progressively reducing biodiversity loss.

This section of our report follows our climate change ambitions and our recent efforts to reduce the environmental impact of Stahl and its value chain partners.

Climate resilience and adaptation

GHG emissions targets and reduction plan

Case study: taking action on climate change

Greenhouse gas emissions

TOPICS

Energy use

“We're always looking for ways to reduce our emissions. In 2023 Stahl Singapore installed more than 1,800 solar panels, reducing the site's dependence on the main power grid by 40% and reducing its scope 2 emissions.”

Michael Costello

Group Director ESG at Stahl

EMISSIONS